Germany’s Energy Transition Makes Room for American LNG

Germany is in the midst of a seismic energy transition. Already in the process of shuttering all its remaining nuclear reactors by 2022, the government is now officially committed to phasing out all of Germany’s coal-fired power stations by 2038. Thanks to the shale revolution, American LNG is poised to fill the void and assist in Germany’s need to reduce emissions.

As Coal Moves Out, LNG Can Move In

Approximately 40 percent of Germany’s power needs are met by plants that burn coal and lignite. And while Germany’s new plan allows for a slow transition away from these fuel sources, it will start with retiring two power plants by the end of 2021, removing 1200MW of capacity from the grid.

The German Federal Ministry for Economic Affairs and Energy has all but assured that a substantial part of this shortfall will be filled with natural gas imports. In the Ministry’s article on Conventional Energy Sources, natural gas is cited as indispensable for a reliable energy supply:

“Natural gas is the second most important primary energy source in Germany’s energy mix, after petroleum. In 2017, its share in Germany’s primary energy consumption amounted to 23.8 percent.”

Germany is the largest economy of the Eurozone, and the region’s largest exporter of goods. The German government has acknowledged its need to diversify its natural gas sources, in order to insulate its economy against geopolitical tensions affecting natural gas imports and ensure that it can keep its industries running during and after the coal phase-out. Germany is looking to, in particular:

- diversify supply sources and transmission routes

- establish stable relationships with supplier countries

- implement long-term natural gas supply contracts and

- develop and maintain a highly reliable supply infrastructure which includes underground storage facilities

Opportunity for U.S. LNG

Germany imports 90 percent of its natural gas, making access to a multitude of suppliers vital to keeping the lights on and the economy moving. Currently, Germany has no LNG Terminals and imports all of its natural gas supply via pipelines – but not for much longer.

The European Commission plans to increase the bloc’s LNG terminal distribution and utilization rate with Germany playing a large role in the infrastructure project. Already, Germany has fast-tracked a LNG terminal project off its northern coast and is expected to add three additional LNG terminals over the next four years. The terminals would increase the EU’s import capacity by a third.

“Utilization rates of terminals in northwest Europe have risen sharply. Uniper, which has an agreement to take LNG from a facility in Freeport, Tex.., said that the shiploads of fuel traded by the company more than tripled from 2017 to 2018, from 40 to 135.”

These new LNG terminals give the United States an opportunity to export its LNG to German consumers and further expand U.S. supply to the entire EU market through Germany’s vast natural gas transportation infrastructure. Germany is even offering supply contracts upwards of 20 years to ensure a reliable supply.

According to Germany’s Ministry for Economic and Energy Affairs, this natural gas will power Germany and other EU member states through Germany’s extensive network of pipelines.

An Ever-Increasing Demand

Germany’s energy options are constrained due to policy shifts in the country and external factors.

After the Fukushima nuclear incident in Japan, Chancellor Angela Merkel announced that all nuclear power plants would be closed within the next decade. This process is expected to be finished by 2022 and will remove approximately 13 percent of energy generation from the grid.

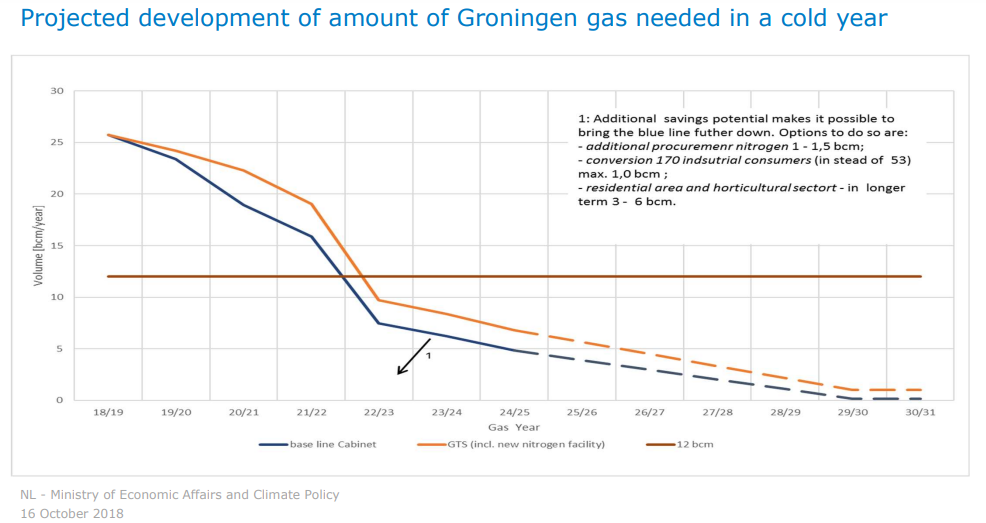

In 2015, the Netherlands supplied 29 percent of Germany’s total natural gas supply – but a decade from now, it won’t supply any. In 2018, the Dutch government announced that it will phase out gas production at its Groningen gas field by 2030. This is slowly reducing natural gas supply to Germany with production in the Netherlands expected to drop below 5 billion cubic meters (bcm) per year by 2025-2026.

This halt in production will account for a decline of 60 percent in European gas supply over the forecast period.

Meanwhile, production and export capacity will only increase on this side of the Atlantic. As International Energy Agency’s Executive Director recently explained:

“The second wave of the U.S. shale revolution is coming. It will see the United States account for 70 percent of the rise in global oil production and some 75 percent of the expansion in LNG trade over the next five years. This will shake up international oil and gas trade flows, with profound implications for the geopolitics of energy.”

This second wave is strengthened by the 338 million cubic meters per day (MMcmd) of export capacity currently under construction and coupled with the 600 MMcmd approved by the Federal Energy Regulatory Commission and not yet under construction.

U.S. LNG and Germany, A Perfect Match

Natural gas will be what moves Germany and the rest of Europe for the foreseeable future. It will keep the lights on, the economy moving and support the European Commission’s ambitious emission targets. With energy options limited by the coal phase out and exacerbated by the withdrawal of nuclear power, along with a decline in the region’s natural gas production, U.S. LNG exporters can look forward to an enduring and mutually beneficial partnership with Germany.

No Comments